Digital Banking vs Traditional Banking: What’s the Future?

Over the past decade, banking in India and across the world has undergone a massive transformation. With the rise of technology, especially after the pandemic, digital banking has moved from being a convenience to a necessity. But does that mean traditional banking is dying? Let’s dive into this ongoing debate to understand what the future holds.

---

What is Digital Banking?

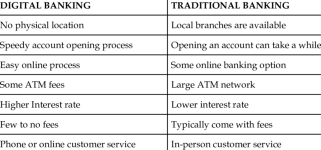

Digital banking refers to the digitization of all traditional banking activities that were historically available only when a customer visited a bank branch. From opening an account to applying for loans or investing in fixed deposits — everything can now be done via apps and websites.

Banks like HDFC, ICICI, SBI, and new-age platforms like Paytm Payments Bank, Fi Money, Jupiter, and RazorpayX are redefining the way people interact with their money.

---

Why is Digital Banking Booming?

There are several reasons why digital banking is gaining massive popularity:

Convenience: No need to stand in long queues or take half-days off work.

24/7 Access: You can transfer money, pay bills, and apply for credit anytime.

Cost-Efficient: Digital operations reduce overheads, leading to better interest rates and lower fees.

Instant Services: From real-time UPI payments to instant KYC verification, everything happens in minutes.

Additionally, the Government of India’s push toward a “Digital India” and the success of UPI (Unified Payments Interface) have accelerated this shift.

---

But Traditional Banks Still Have a Role

Despite the rise of digital services, traditional banks still offer significant value:

Personal Relationships: Many customers, especially in Tier 2 & 3 cities, value face-to-face interactions.

Trust & Security: Older generations often trust physical branches more than online platforms.

Complex Services: Business loans, mortgages, and legal verifications often still require in-person consultation.

For example, a large business loan may require discussions, multiple documents, and legal assessments — which are easier to manage through a branch manager.

---

Challenges Faced by Digital Banking

Cybersecurity: Digital platforms are more exposed to hacking and fraud.

Digital Literacy: Not everyone is comfortable using smartphones or understanding digital terms.

Internet Dependency: Without stable connectivity, services can be inaccessible.

---

Hybrid Model: The Likely Future

Instead of one completely replacing the other, the future is likely to be a hybrid model, where banks provide both strong digital interfaces and reliable offline support. Most top banks are already investing heavily in both.

---

Conclusion

Digital banking is undoubtedly the future — it’s faster, cheaper, and accessible. However, traditional banking still holds its ground, especially when it comes to trust and complex services. The smartest move for banks would be to merge the two worlds — offering digital-first experiences without removing the human element entirely.

As we move into 2025 and beyond, banks that adapt fastest to this new hybrid model will win the trust (and wallets) of India’s next generation of customers.

-------

Over the past decade, banking in India and across the world has undergone a massive transformation. With the rise of technology, especially after the pandemic, digital banking has moved from being a convenience to a necessity. But does that mean traditional banking is dying? Let’s dive into this ongoing debate to understand what the future holds.

---

What is Digital Banking?

Digital banking refers to the digitization of all traditional banking activities that were historically available only when a customer visited a bank branch. From opening an account to applying for loans or investing in fixed deposits — everything can now be done via apps and websites.

Banks like HDFC, ICICI, SBI, and new-age platforms like Paytm Payments Bank, Fi Money, Jupiter, and RazorpayX are redefining the way people interact with their money.

---

Why is Digital Banking Booming?

There are several reasons why digital banking is gaining massive popularity:

Convenience: No need to stand in long queues or take half-days off work.

24/7 Access: You can transfer money, pay bills, and apply for credit anytime.

Cost-Efficient: Digital operations reduce overheads, leading to better interest rates and lower fees.

Instant Services: From real-time UPI payments to instant KYC verification, everything happens in minutes.

Additionally, the Government of India’s push toward a “Digital India” and the success of UPI (Unified Payments Interface) have accelerated this shift.

---

But Traditional Banks Still Have a Role

Despite the rise of digital services, traditional banks still offer significant value:

Personal Relationships: Many customers, especially in Tier 2 & 3 cities, value face-to-face interactions.

Trust & Security: Older generations often trust physical branches more than online platforms.

Complex Services: Business loans, mortgages, and legal verifications often still require in-person consultation.

For example, a large business loan may require discussions, multiple documents, and legal assessments — which are easier to manage through a branch manager.

---

Challenges Faced by Digital Banking

Cybersecurity: Digital platforms are more exposed to hacking and fraud.

Digital Literacy: Not everyone is comfortable using smartphones or understanding digital terms.

Internet Dependency: Without stable connectivity, services can be inaccessible.

---

Hybrid Model: The Likely Future

Instead of one completely replacing the other, the future is likely to be a hybrid model, where banks provide both strong digital interfaces and reliable offline support. Most top banks are already investing heavily in both.

---

Conclusion

Digital banking is undoubtedly the future — it’s faster, cheaper, and accessible. However, traditional banking still holds its ground, especially when it comes to trust and complex services. The smartest move for banks would be to merge the two worlds — offering digital-first experiences without removing the human element entirely.

As we move into 2025 and beyond, banks that adapt fastest to this new hybrid model will win the trust (and wallets) of India’s next generation of customers.

-------